Synthetix v3 to bring in a new era of decentralized finance

Synthetix Research Report October 2023

Key Takeaways:

perps v2 has already surpassed $27bn in volume and distributed over $22m in fees to stakers

based on existing markets only, SNX is trading at a historically low PE multiple of ~19x

v3 upgrade is a significant catalyst that will increase volume and revenues materially over the coming 12 months

Hybrid exchange ‘Infinex’ on v3 expected to provide a new standard of user experience to compete with DYDX and major CEXs

Picolo Research target a price range for SNX between $13.00 and $22.00 by 2025.

Download the PDF version here

Disclaimer

Picolo Research or/and its team hold positions in SNX, DYDX and GMX. This report is not to be construed as financial advice. While we do our best to ensure that the data within this report is accurate, we cannot guarantee that mistakes are not made either by us or the data providers that we utilize. Please do your own due diligence.

v2 - a battle-tested stepping stone to something bigger

Synthetix, a project that has been through several iterations since mid 2017, is a liquidity layer used for powering decentralized derivatives and finance applications. In the same way in which Ethereum is the foundation for creating smart contracts, Synthetix aims to be the building blocks for DeFi.

Synthetix v2 has proven to be battle-tested infrastructure for a handful of perpetual futures and derivatives markets. Several front-ends (markets) including Kwenta, Polynomial, Lyra Finance and Thales have processed billions of dollars in derivatives transactions using Synthetix liquidity, while simultaneously rewarding stakers through the distribution of trading fee revenues.ᅠ

Since the downfall of FTX, competition in the perpetual dex arena has been aggressive. Hybrid solutions such as DYDX continue to dominate the user acquisition and volume game, however, order books and the matching system remain centralized, skewing the data for the purpose of this analysis.

On the more ‘pure-dex' side, GMX, Gains Network and Synthetix powered Kwenta are currently the top three contenders pushing the most volume, and as a result, the highest distribution of revenue to stakers.

The fee-sharing narrative is alive gaining traction

Despite the drop-off in perp dex volumes since the end of Q1, Synthetix has continually gained a larger slice of the fee revenue, currently second in place to GMX.

Annualizing SNX average fees over the last month equates to around $39m which will be distributed to stakers over a year. This brings the current PE ratio based on a circulating supply of 323m tokens and a price of $2.05 to ~19x multiple.

It’s worth noting that Synthetix v2 has operated as a product, plugging into select front-ends to provide a simple liquidity service. The launch of the much anticipated v3 however, transforms Synthetix into a platform, providing the infrastructure for significantly more than just pure liquidity, and as a result, much higher revenues.

More on this later in the research.

The launch of v3 and the race to the ‘End Game’

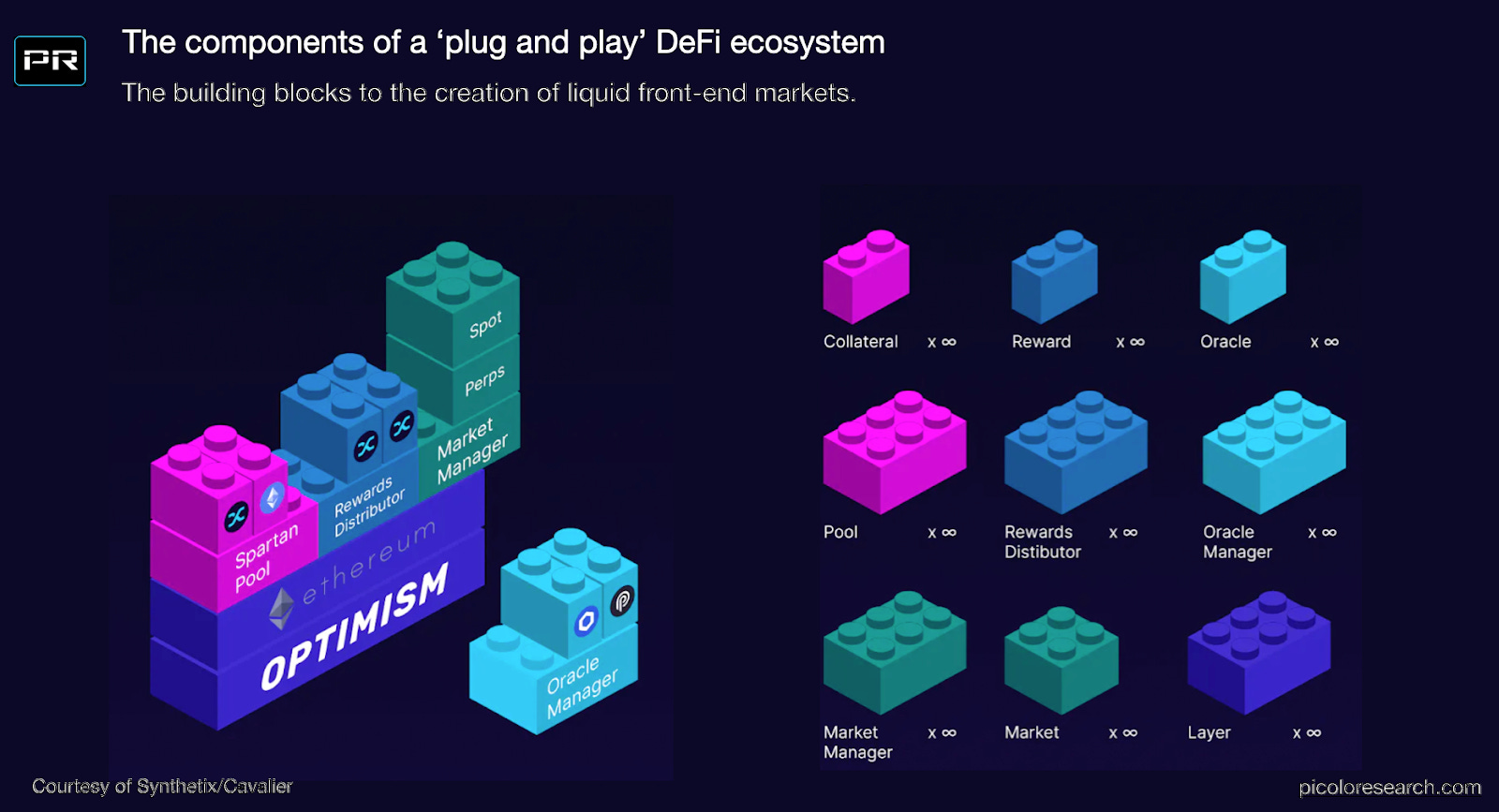

Synthetix v3 will operate as the base layer of future defi applications through the integration and availability of Markets and Pools.

Markets are the ‘front-ends’ that launch on top of the Synthetix infrastructure layer, while ‘pools’ are the source of decentralized liquidity provided by LP’s seeking yield. The availability of these two components opens the door to endless possibilities of DeFi applications.

Consider the following as an example:

A founder wants to launch a platform for Binary Options trading.

As of right now, the founder would need to:

> Build a front end

> Create decentralized options and derivatives contracts for each instrument

> Integrate with oracles for pricing and data feeds

> Create vaults to collateralize the derivatives

> Sufficiently price the vault yield to match the corresponding risk

> Market the vaults to bring in capital so the options trades are sufficiently collateralized

If the founder was to use Synthetix v3 as the base liquidity layer, the process of building this Market would be the following:

> Build front end (Market)

> Setup required Oracle via Chainlink or Pyth

> Propose Pool to Synthetix Spartan Council (Pool)

> Once approved, tap liquidity from SNX

The v3 journey significantly cuts down build time and operational output by streamlining the highly complicated issues of creating such derivatives from scratch, pricing and attracting the necessary LP capital to operate them.

In traditional markets this type of relationship is commonly referred to as ‘whitelabel’, an arrangement in which most of the infrastructure and demanding operational work is provided by one company, and subsequently licensed to unlimited third parties that seek to build a front-end and market it for a slice of the revenue.

Other than the fact that it is decentralized, a considerable difference between traditional whitelabelling and Synthetix v3 is the sheer amount of flexibility available in creating new verticals of markets that may not yet even exist.

Over the last few years, traders and market participants have become accustomed to certain features in centralized exchanges and marketplaces that until now have been unable to move over to the realm of decentralized offerings. Synthetix v3 encompasses numerous upgrades that give the platform a real shot at being a contender versus its centralized counterparts.

Multi collateral trading; essentially using any liquid assets that can be sufficiently priced by an oracle as collateral for trading in perps

Cross margin trading; allowing traders to take multi-legged long/short trades in a margin efficient manner and without requiring extra collateral

The ability to trade on any EVM; v3 can be deployed on any compatible EVM

Efficient Cross-Chain liquidity - Utilizing cross-chain teleporters to speed up and simplify the process of rotating capital to different chains

Permissionless listing of tradable instruments; though at first anticipated to be approved by Synthetix Council, listing of new assets may be permissionless

Enter Infinex, Synthetix answer to an exchange for the masses

The team at Synthetix have openly talked about the friction in onboarding new users to decentralized exchanges. The handling of private keys, bridging to various layer-2’s and the endless signing of transactions on-chain provides enough barriers to deter any prospect that is unfamiliar with self custody.

Infinex, a front-end perp market built on Synthetix v3, is anticipated to launch in late 2023 as a ‘hybrid’ solution to meet the needs of the average retail trader. Though at its core it is decentralized, various technological compromises are to be made to give the platform the ‘feel’ of it being centralized and in the same league as CEX market leaders Binance and OKX.

Some of these hybrid features include:

Signup/login using traditional methods (email, 2FA etc)

Multichain deposits

Withdrawal passwords and whitelists

Account recovery/ exchange MFA key backups

KYC only for users seeking to onramp fiat

No requirement for signing of transactions/ instant interactions

Essentially, the goal of Infinex is to streamline the onboarding and user experience to a point in which the user is almost unaware that they are trading on a decentralized exchange.

Comparing apples and oranges

This report has largely omitted data from DYDX thus far for two reasons being 1) its current iteration (v3), does not implement any fee sharing to its token holders and 2) DYDX handles a core part of the protocol in a completely centralized way through its implementation of an off-chain orderbook. While these components may be modified in the future (v4), the details are currently lacking.ᅠ

For the purpose of illustrating valuation of SNX, we will look towards how the network brings in revenue, as well as where this ranks in comparison to its peers. For this exercise, we will assume that DYDX give 100% of fees to stakers.

*As of 25 Sep 2023, Source: Coingecko, Token Terminal

Even in its current iteration of v2, Synthetix fee revenue has picked up substantially in the second half of this year. 90-day fees are 30% below DYDX, but well ahead of GMX for the same period.

Risk management leads to superior profitability

Synthetix distinguishes itself from other platforms not merely by its fee structure but primarily through its innovative product design that promotes superior risk management and market neutrality. This is achieved through two distinct mechanisms: the Dynamic Funding Rate and the Price Impact Function.

The Dynamic Funding Rate ensures delta neutrality by incorporating velocity of skew in addition to the conventional market skew. This counteracts any sustained long skew by progressively increasing the funding rate, thereby prompting traders to counterbalance the market and swiftly restore equilibrium.

Conversely, the Price Impact Function considers the depth of the order book to modify the execution price based on trade size and the prevailing market skew, thereby incentivizing traders to position themselves in a manner that reduces the skew.

Collectively, these functions are pivotal for robust risk management, as they work cohesively to diminish LP (stakers) risks, curtail prolonged skew, and ensure market neutrality. In short, this concept is akin to lowering the max drawdowns of one’s investment portfolio, which is a measure of downside volatility.

SNX trades at a PE of ~19x

When comparing Fees as a percentage of Fully Diluted Valuation (FDV), Synthetix has a PE Ratio of ~19.35, considerably better than its peers.

Some may argue that the PE/Ratio should be based on circulating supply/market cap given that only unlocked tokens are able to receive such fee sharing. In this instance, DYDX comes in with an extremely low and attractive PE of 6.28, however this doesn’t take into account the hefty amount of token emissions on the horizon.

As of today there are around 180m DYDX tokens in circulation. In six months time, this number is going to quickly grow to 545m, significantly inflating the supply and corresponding market cap.

Even on a PE basis with the additional forecasted token emissions, DYDX has a healthy financial profile for investment, however the impending distribution the future tokens to seed investors is cause for concern given where we are at in the current market cycle. We would anticipate that there will be large liquidations by some investors, further dampening the price.

Synthetix (SNX) on the other hand, has a total supply of 324m tokens and a circulating supply of the same. Outside of token inflation that occurs (which 100% is distributed directly to stakers), there are no further unlocks to be had.

Can SNX take a meaningful slice of the market?

It’s no secret that trading volumes are vastly down from their heights in 2021 and 2022, so it makes sense that token prices, as a reflection of this activity, are also trading down 70-90% from their highs.

Where things get interesting is predicting where such token prices will be once perp and trading volumes begin to recover given that real fee-sharing mechanics are now in force.

We can extrapolate the potential of volumes and therefore corresponding token valuations by two methods, neither of which is perfect, but it gives a solid foundation for where things are and where they could be.

SNX Market Share of Total Centralized Derivatives Market

We are optimistic that decentralized derivatives exchanges will continue to eat into the marketshare of CEX’s as UI and onboarding becomes more streamlined for the masses.

Looking back since the start of the bull market, we observe that derivatives volume averaged ~$85b per day, and since then, has dropped about 18% through 2023.

If we are to look at what level SNX is currently operating at as a percentage of total CEX volume, it barely registers a blip at ~0.21%. While this currently looks good from a fee-sharing point of view, for SNX to be a real competitor in the global derivatives space, maintaining their current position in the race and relying on a ‘rising tides lifts all boats’ scenario is not an option.

The ultimate goal should be to further penetrate the existing/total derivatives market at all costs, with hopefully v3 being the catalyst to do so.

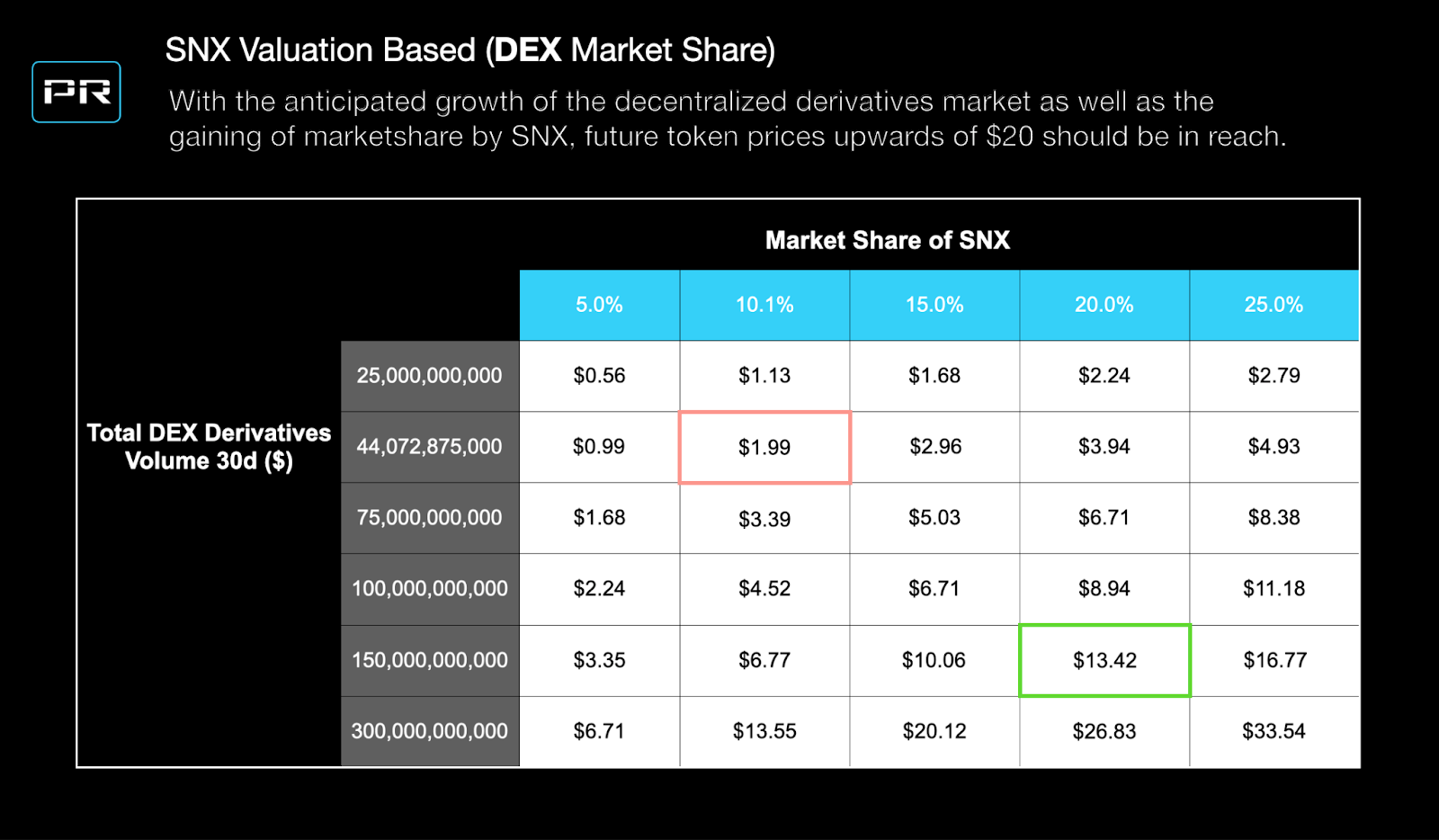

SNX Market Share of DEX Derivatives

Perhaps more appropriate in forecasting potential valuation is looking at where SNX sits in relation to its competitors and the growing decentralized sector itself. Current DEX derivatives volumes are around ~$45b per month across the top exchanges mentioned in this report. At a ~10% marketshare through the current front-ends of Kwenta, Polynomial, Lyra etc, Synthetix trades at a price of around $2.00.

We expect that by 2025, total DEX derivatives will exceed 150b per month, with SNX related markets conservatively commanding a 20% marketshare based on a surge of v3 integrations in derivatives and gamblefi markets. This is our bear case.

SNX stakers remain loyal throughout the bear

The bear market has culled most traders and transferred ownership to those looking longer term. As of writing, approximately 84% ($560m) of all SNX is currently staked between L1 and L2.

This makes for an interesting scenario in terms token supply dynamics for when demand for SNX is high. With little circulating tokens available (16%) and perceived strong demand for income producing tokens at launch of v3, it is likely that even moderate amounts of buy pressure will lead to a significant move to the upside.

Potential risks in SNX growth

There’s a few aspects that are worth noting that can impact the success of SNX over the short term.

DYDX is an excellent competitor with strong leadership that will likely do very well over the coming years. Despite its shortcomings mentioned previously relating to upcoming token emissions, there is no doubt that their volume has been impressive and is a considerable goal for SNX to aspire to with its release of v3.

While DYDX may maintain a market lead for the foreseeable future, we believe the DEX market to be large enough to have several robust players tackling different aspects of the ecosystem.

The launch of Infinex, whilst being a huge milestone for SNX, may pose some regulatory risk, albeit its very unclear at this point. Hybrid exchanges generally have corporate structures that deal with KYC, fiat onramps and other centralized services which expose them to market oversight by global regulators. While Infinex is entirely separate to Synthetix, we would still likely see some indirect negative effects on the price of SNX should regulatory issues arise. A more accurate assessment can be made on this risk closer to launch.

Beyond its primary Ethereum-based operations, another significant challenge confronting the SNX platform is the limited activity of users on its secondary chains, Optimism. While GMX has witnessed substantial user engagement on Arbitrum, Optimism has recorded only half the daily active users (DAU) in comparison over the past six months. Such disparities in user activity could decelerate SNX's adoption rate in the short term, or until cross-chain activities bear fruits. SNX founder Kain has recently shared his vision on cross-chain liquidity, a huge step in the right direction that will likely begin with deploying on Base.

Lastly, there are various technical risks associated with such a major upgrade to v3. This report does not make an analysis of such risks, however we expect that third-party audits will be made available prior to launch.

The fastest horse in the race

We believe that several new major narratives are currently in the making, and SNX is a top contender to benefit from them over the next cycle.

Rising from the carnage of 2022, decentralized trading experiences will continue to gain popularity. The only thing that has more upside than a world-class trading product is a complete liquidity network that powers an ecosystem of its own. As speculators increasingly shift away from centralized venues, demand for decentralized derivatives markets will reach new highs. The ‘plug and play’ building experience on SNX v3 has the ability to power an array of different markets and instruments while feeding all the benefits and value accrual back to the token holder. The DEX narrative is still in its infancy and will likely grow with the release of more hybrid solutions such as Infinex.

For the first time in crypto, we are also finally witnessing the rise of tokens that provide yield, dividends or some type of value back to tokenholders. Ironically, the best of these tokens have existed for some time, and we believe SNX to be one of the most attractive. Trading under a PE of 20, its current valuation is more reasonably priced than most speculative tech companies on the NYSE. Of course, there are inherent risks associated with crypto that are not to be understated, however in the allocation of capital to the sector, we find such income bearing assets to be particularly attractive in the current environment.

Lastly, this report so far has omitted a review of the SNX team given that it has changed considerably over time and become more decentralized and distributed in its decision making. Despite this, it’s worth noting that the leadership behind SNX has a track-record of experimentation and execution that leads to results. Equally as impressive is their timing on implementations of their solutions within market cycles. Synthetix was one of the earliest tokens that propelled the 2020 DeFi bull market into existence. With the data we have at hand and the activity levels we have observed of the team and network over the past six months, we foresee Synthetix once again climbing the ranks of the top 100 in 2024.

Our target range for SNX is between $13 and $22 by 2025.

Read the full report in PDF format here